Authorised IT Filing Platform by Indian Income Tax Department 4.8 ★★★★★ Excellence since 2016

4.8 ★★★★★ Excellence since 2016

4.8 ★★★★★ Excellence since 2016Home > Income Tax > Help Center > Section 134 (Section 80GG)

Section 134 (aka Section 80GG) is a deduction under Chapter VIII (aka Chapter VI-A). This section provides relief to those taxpayers who are not in receipt of house rent allowance (HRA) but pays rent for their residential purpose.

This document covers

The following conditions needs to be satisfied for claiming deduction u/s 134 of IT Act 2025 (u/s 80GG of IT Act 1961)

The deduction will be the least of the following.

Mr Ram, a businessman, has a gross total income of Rs 460000. He is paying a rent of Rs 12000 per month. What is the amount of deduction available u/s 134 (aka u/s 80GG)?

As Rs 60000 is least of above, 60000 is the deduction u/s 134 (aka u/s 80GG).

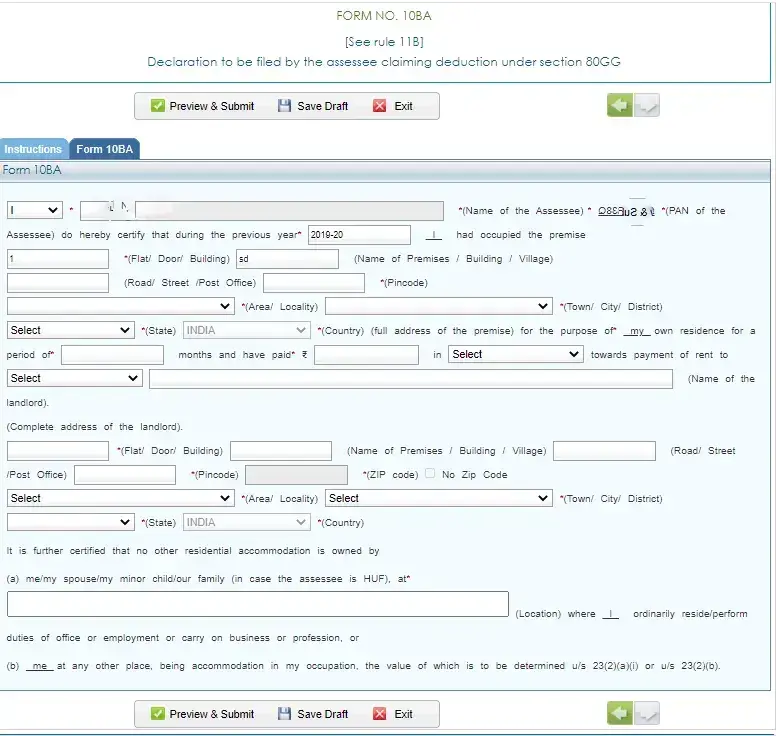

If the taxpayer wants to claim deduction u/s 134 (aka u/s 80GG), he/she needs to submit 📄Form 31, aka Form 10BA in Income tax e-filing portal as a supporting document. The following are the details in 📜Form 39 of IT Act 2025 (Form 10E of IT Act 1961).

The taxpayer claiming deduction towards rent paid u/s 80GG should submit 📄Form 31, aka Form 10BA in Income Tax portal before ITR eFiling. Otherwise rent paid u/s 134 (aka u/s 80GG)will be disallowed as deduction

Sample 📄Form 31, aka Form 10BA

Disclaimer: This article provides an overview and general guidance, not exhaustive for brevity. Please refer Income Tax Act, GST Act, Companies Act and other tax compliance acts, Rules, and Notifications for details.